Uber, the ridesharing company that is taking over the taxi industry by storm, is all over the headlines these days. Founded in 2009, the company has since expanded to 36 countries and is doubling revenue every 6 months.[1] Backed by influential investors including Google Ventures, Goldman Sachs, and Jeff Bezos, Uber completed its latest round of funding in June with a valuation of $17 billion.

The taxi industry is usually highly regulated, restricting the number of taxis operable at any given time. Given Uber’s similarity to a standard taxi, it should be no surprise that the company is the target of numerous lawsuits. Demonstrations have been held and Ubers cars have even been attacked by taxi drivers during protests.[2] Legal issues aside, the company is welcomed by both taxi riders and Uber drivers thus far.

So why is Uber loved by most people? Along with cheaper fares, Uber also offers a review system where its drivers are rated according to customer satisfaction. In addition, Uber claimed that Uber drivers earn significantly higher than regular taxi drivers.[3] Combine all of these factors and you get a company that is seemingly working to better the taxi industry for both users and drivers.

But will the future be what its proponents think it will be? Will Uber continue to deliver? The answer is no. Uber’s high margins, increased revenue for drivers, and cheaper fares are mutually exclusive and will be short lived.

Uber’s rapid growth is the result of integrating GPS into its fleet, thereby increasing efficiency, and removing the cap on the supply of drivers. The bulk of economic value that Uber contributes to the industry is the increase in utilization (increase in productivity). As a result, we see a rise in average revenue per driver (ARPD) as waiting times are reduced. Uber then passes some of the savings resulting from this increase in efficiency to the consumers, decreasing the fare. This creates the illusion of a virtuous cycle, as illustrated below by Mr. David Sacks.[4]

Before we delve further, I would like to make two reasonable assumptions about the industry.

Before we delve further, I would like to make two reasonable assumptions about the industry.

- There is a large supply of drivers

- Ridesharing companies will compete in the same city (we are seeing this already)[5]

As prices decrease, the optimum will eventually be reached, and further decreases in the price would be uneconomical. However, Uber will still be pressured to recruit more drivers when it reaches that point. Why? If I may borrow Mr. Bill Gurley’s (an Uber investor) article: the network effect is the name of the game. It improves pick-up times, increases coverage density, and ultimately increases utilization. So how can Uber increase its network effect? One key variable is the number of customers (demand), and since price is fixed at the optimum, the only other input would be the number of drivers.

Unfortunately for Uber, the low barriers to entry implies fierce competition, we are already seeing a multitude of ridesharing companies: Lyft, Sidecar, Summon, just to name a few. Due to competition, every company has an incentive to recruit more drivers to increase its own network effect. This is the beginning of a vicious cycle.

Each company will face constant pressure to recruit more drivers. In doing so, the overall utilization and ARPD of the industry will decrease. As more drivers sign up for Uber, the inevitable equilibrium is one where the ARPD will be at its minimum. As drivers’ revenue decreases, riders will also suffer from poor service.

Can’t Uber just fend off competition with its established fleet already? It is possible if Uber can somehow establish brand loyalty. However, it is highly unlikely considering that its service acts like a commodity, much like the commercial airline industry.

The $17 Billion Valuation

People rave about how fast Uber is growing, how Uber is creating jobs, and how Uber will expand into alternative markets. The exact market share that Uber will have is highly debatable. Mr. Aswath Damodaran, a renowned professor at NYU Stern, recently wrote an article questioning the potential market for Uber. Mr. Bill Gurley then wrote the aforementioned article in response. While the total market size is important, I believe that Uber’s operation should be scrutinized to determine its true growth potential and profitability in the long run.

Uber essentially places a GPS on a car, and voila, its owner becomes an Uber driver. The information from the GPS is then relayed to the rider’s app, where the rider can hail an Uber car. During the ride, the GPS is again used to calculate the total fare, set by Uber.

First of all, the technology used isn’t new. Without patents to protect itself, how can Uber sustain the current margin? Secondly, Uber’s continued operation is controversial because it violates the intended goals of taxi regulations around the world. In fact, the only reason Uber expanded so quickly was because its deep pockets allowed it to waltz into any city and start operating, regardless of any laws. When being investigated, Uber can throw cash at lawyers until a favourable verdict is reached.[6] This isn’t exactly what I would call good business practice.

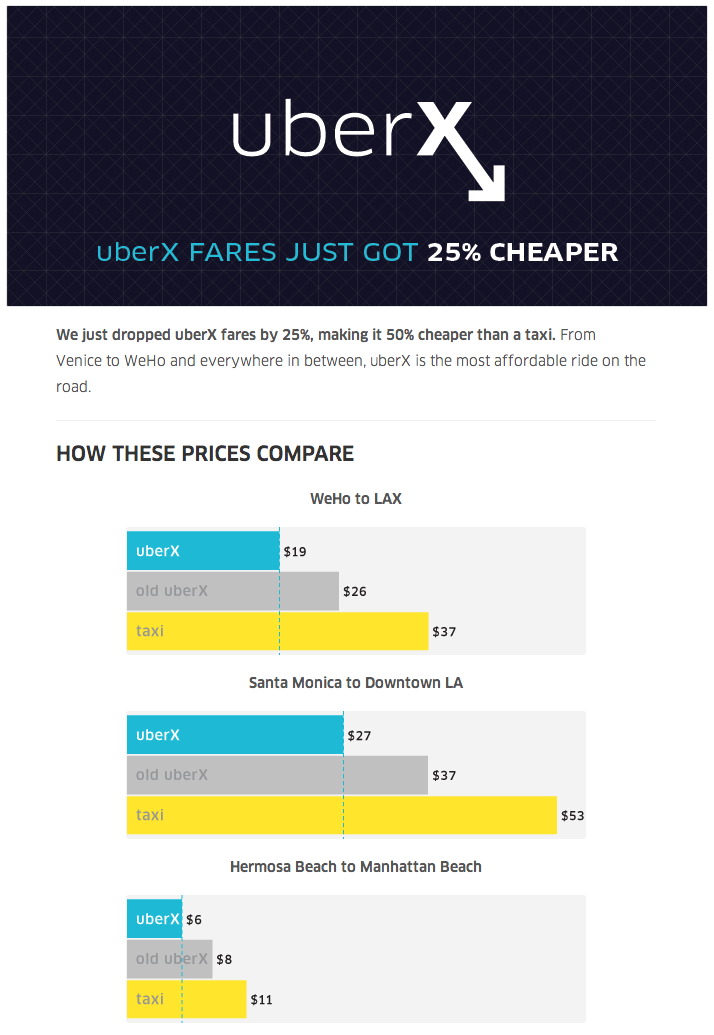

We established previously that Uber will continue to face hiring pressure. Well that can’t go on forever, because the ARPD will decrease to the point where no driver will work for you. Uber cannot increase the price either because that would decrease the total revenue (deviation from the optimum). Uber can try to remedy this problem only by decreasing its own cut of the fare. Thus we can see that the current commission of 20% will not be feasible in the future. In fact, the price war between ridesharing companies has already prompted Uber to take a loss on rides following this update.

But is Uber worth $17B? On one hand, Uber is still bringing in huge amounts of cash at little to no variable cost. Without any need for capex, Uber may continue to expand at a rapid pace. However, the same holds true for other ridesharing companies. In the long run, ride sharing companies will operate with razor thin margins, as each company struggles to keep fares low and drivers happy. In addition, the fact that governments around the world are starting to ban ridesharing companies isn’t helping Uber’s case either. [7],[8],[9]

I do not know how the VCs valued Uber, but I believe that any valuation for Uber should place heavy emphasis on cash flows in the coming years. If the $17 Billion valuation is based on Uber’s cash flows down the line while assuming the current margin and growth rate, then investors should be in for a tough ride.

[1] http://blogs.wsj.com/digits/2014/06/06/uber-ceo-travis-kalanick-were-doubling-revenue-every-six-months/

[2] http://techcrunch.com/2014/01/13/an-uber-car-was-attacked-near-paris-as-taxi-drivers-protest-against-urban-transportation-startups/

[3] http://abovethecrowd.com/wp-content/uploads/2014/07/Screen-Shot-2014-07-07-at-6.41.45-PM.png

[4] https://twitter.com/DavidSacks/status/475073311383105536

[5] http://www.forbes.com/sites/quora/2014/06/10/whos-winning-right-now-in-the-competition-between-lyft-and-uber/

[6] http://techcrunch.com/2013/01/31/a-day-after-cutting-a-deal-with-lyft-california-regulator-reaches-an-agreement-with-uber-as-well/

[7] http://mashable.com/2014/07/21/seoul-korea-bans-uber/

[8] http://www.telegraph.co.uk/news/worldnews/europe/germany/10991089/Hamburg-breaks-ranks-and-bans-Uber-app.html

[9] http://www.engadget.com/2014/04/15/belgian-uber-ban-10k-fines/

{kind=link}